9 however, federal tax law provides the personal representative of the surviving spouse’s estate with a claim against the remaindermen for the estate taxes attributable to the. A testamentary direction to pay debts, charges, taxes, and expenses of administration is not considered to be a direction against statutory estate tax apportionment.

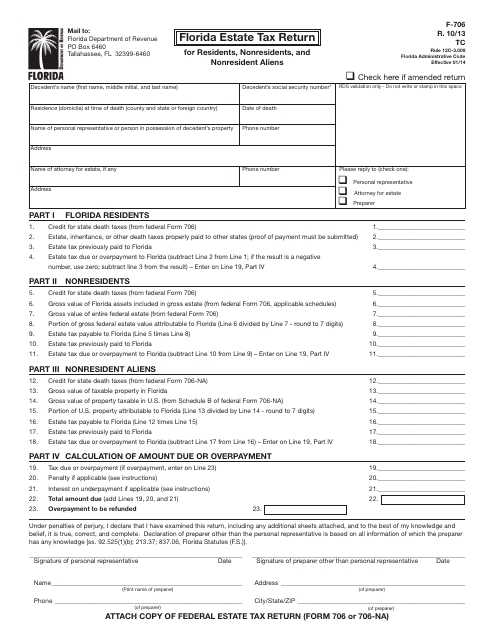

Form F-706 Download Printable Pdf Or Fill Online Florida Estate Tax Return For Residents Nonresidents And Nonresident Aliens Florida Templateroller

Florida law provides that the default allocation and apportionment of estate taxes is that the recipient of insurance and other nonprobate assets pay their share of the estate taxes attributable to those nonprobate assets, absent a proper allocation of those taxes to probate property.

Florida estate tax apportionment statute. (d) “gross estate” means the gross estate, as determined by the internal revenue code with respect to the federal estate tax and the florida estate tax, and as that concept is otherwise determined by the estate, inheritance, or death tax laws of the particular state, country, or political subdivision whose tax is being apportioned. Inordinate as it might appear, due 3) imposes upon the residuary portion of a trust the taxes on specific distributions and 4) provides that federal law.

(de) “included in the measure of the tax” means that for each separate tax that an interest may Generally speaking since most florida residents die with less than the applicable exclusion amount, florida’s tax apportionment statute will only apply to a small percentage of florida estates. If the net tax paid to another state is greater than or equal to the tentative florida tax attributable to the property subject to tax in the other state, none of the florida tax shall be attributable to that property.

(1) (a) except as provided in paragraph (b), the tax base of an insurance company for a taxable year or period shall be apportioned to this state by multiplying such base by a fraction the numerator of which is the direct premiums written for insurance upon properties and. This statute hasn’t been substantially revised since 1998, although a number of significant changes have occurred in federal and state tax laws since that time, including the elimination of the federal credit for state death taxes and, by extension, the. Improvements made to floridas estate tax apportionment statute author:

Federal estate tax apportionment the federal estate tax' is not a tax on property or on the right to receive property from a decedent; As to any simple estate plan that is subject to death taxes,6 the statute apportions death taxes quite easily. Respect to the federal estate tax and the florida estate tax, and as that concept is otherwise determined by the estate, inheritance, or death tax laws of the particular state, country, or political subdivision whose tax is being apportioned.

Rather it is a tax on the privilege of transferring property from the dead to the living. 179 (d) 180 “gross estate” means the gross estate, as determined by the internal revenue code with respect to the federal estate tax and the florida estate tax, and as that concept is otherwise determined by the estate, inheritance, or death tax laws of the particular state, country, or political subdivision whose tax is being apportioned. Improvements made to florida’s estate tax apportionment statute the tax on such interests will be apportioned in the manner provided for interests passing from the estate or the trust.14 common instrument construction.

(e) preparation of the estate’s federal estate tax return. The decedent's last will provides: Under the trust, the will should provide that estate tax apportionment shall be determined in accordance with the terms of the trust.

(c) the reduction in the florida tax on the estate of a florida resident for tax paid to other states shall be allocated as follows: (d) “gross estate” means the gross estate, as determined by the internal revenue code with respect to the federal estate tax and the florida estate tax, and as that concept is otherwise determined by the estate, inheritance, or death tax laws of the particular state, country, or political subdivision whose tax is being apportioned. 2) sets forth a more stringent standard to direct against statutory apportionments;

1) specifies that language must be inserted in the will if the executor is looking to the trustee of the decedent's revocable trust to pay the estate taxes; The uniform estate tax apportionment act (the uniform act). Consistent with the concept of equitable apportionment, the uniform act directs that estate tax be apportioned to the gross

Price's athored article for summer 2015 issue of actionline created date: When estate taxes are due in the surviving spouse’s estate, the remaindermen may argue that, according to florida law, they are not required to contribute estate taxes attributable to the homestead. 733.817, and it’s notoriously complex and tricky to apply.

Under the prior apportionment statute, a decedent’s will.

4th Dca When Does A Surviving Spouses Elective Share Take An Estate-tax Hit - Florida Probate Trust Litigation Blog

Scholarshiplawuncedu

Floridafellowsinstituteorg

Pdf Format - American College Of Trust And Estate Counsel

Flsenategov

Flsenategov

Jstororg

2

New Florida Homestead Laws Add Flexibility In Estate Planning - Pdf Free Download

Improvements Made To Floridas Estate Tax Apportionment Statute In Actionline Dean Mead

2

2

2

Does Your State Have A Throwback Rule Or A Throwout Rule

2

Flsenategov

Katzbaskiescom

Floridafellowsinstituteorg

Legstateflus